.jpg)

Spend a few minutes each day completing a task in our budget organizer. After 10 days, your finances will be in spring-clean working order! Wash, Rinse, Repeat: Once yearly. (Or more, we won’t tell!)

Budget Organizer Day 1: Re(dis)cover online banking

Make sure you know your username and password for online banking for all of your accounts.

If you don’t, recover them by clicking ‘forgot password’ and following the prompts. Here’s a checklist of the ones to make sure you have active access to. Check them off when complete.

- Retirement Accounts

- Checking Accounts

- Savings Accounts

- HSA/FSA Accounts

- Auto Loan

- Mortgage

- Other Loan

- Credit Cards and Retailer Credit Cards

Budget Organizer Day 2:

Security Checkpoint!

If anything in your life should have iron-clad security, it's your money. Implement these tips to ensure your household finances are secure.

- Get a free password manager to safely store all of your usernames and passwords. Reputable ones include LastPass, BitWarden, and 1Password, to name a few.

- Don’t reuse the same password more than once.

- Don’t share passwords.

- Include upper and lowercase letters, numbers, and symbols in your passwords.

Pro tip: adding a blank space with your spacebar in the middle of a password (if the system allows it) makes it infinitely more difficult for hackers to crack. - Don’t use family members’ names or pet names, and don’t use your date of birth or other significant ‘easy to guess’ items in your passwords.

- Check out if a specific password has been hacked at haveibeenpwned.com/Passwords.

Budget Organizer Day 3:

App It Up

Now that you have all of your usernames and passwords updated and stored, it’s time to get each bank or credit union's app for your mobile devices.

.png?width=500&name=10%20day%20budget%20tidy%20up%20checklist%20images%20(2).png)

Why? Because they're designed specifically for easy use on mobile! And that makes them more secure than using your internet browser. It’s worth searching the App Store or Google Play to see if each of your financial institutions has an app. (They probably do.) Setting up FaceID or TouchID will make it even easier. Then put all your bank apps in a folder on your phone or tablet titled "Finance" to make them easy to find. The best part is that you can complete this budget organizer item without getting off the couch!

Budget Organizer Day 4:

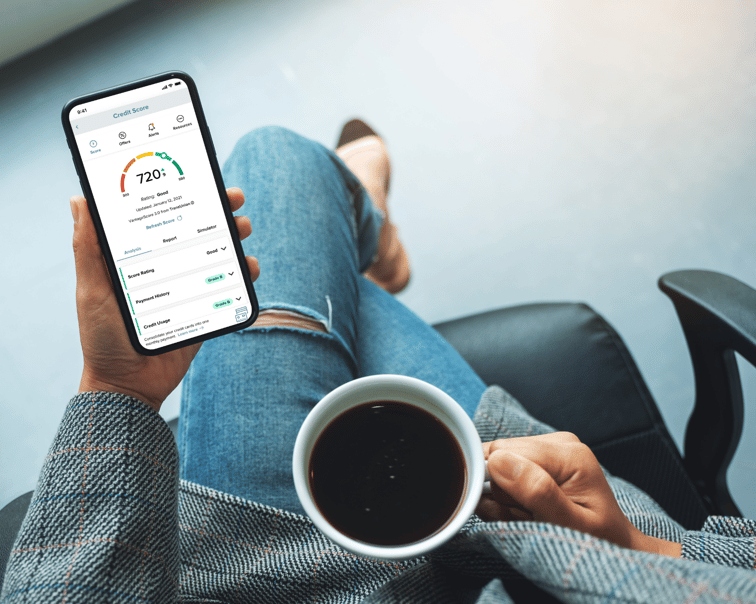

Credit Check on Aisle 5

Set yourself up for success by enrolling in the free credit score tool within Copper State Credit Union Online Banking.

You'll get daily updates on your credit score as well as credit report changes and real time credit monitoring. All without doing a hard pull on your credit. Learn more here, or just log in to your Copper State Credit Union online banking and enroll in Free Credit Score!

Also - know that you’re legally entitled to a credit report from all three agencies (TransUnion, Equifax, and Experian) once per year. You can find this at AnnualCreditReport.com – the only source for free credit reports from all three agencies and authorized by federal law.

Once you get your report:

- Check for errors (1 in 5 Americans 😵 has an error on at least one of their credit reports).

- Dispute errors if needed. Here's a guide from the CFPB on the most common errors and how to fix them.

Budget Organizer Day 5: Statement, Shmatement

Enroll in electronic statements, if you haven't already.

-4.gif?width=650&height=200&name=Untitled%20design%20(2)-4.gif)

You know bank statements are important, but they’re mailed to you each month and then strewn all over your house/apartment/file cabinet/junk drawer/cat’s litter box/recycle bin...need I continue?

They’ll be much safer electronically filed away. So take care of this for your family budget, sign up for eStatements and make your life a little more clutter-free. Plus, enrolling in eStatements saves you the $2 per month Paper Statement Fee (our cost for mailing).

“But I’m already enrolled in eStatements”

Awesome! How long has it been since you downloaded them and filed them in a folder on your computer? For security reasons, eStatement PDFs aren't sent as an attachment to your email inbox, but instead are stored securely within your online banking. So, take 15 minutes, blast your favorite 90s playlist and knock out this budget tidy-up task in no time. Then you’ll be prepared when you need to refer to these statements in the future - i.e. tax time or when you're applying for a mortgage loan.

Budget Organizer Day 6:

Red Alert

Almost every bank and credit union have some type of text or email alert/notification system. Your budget organizer process should include adding at least one or two alerts. These notifications let you know when something happens on your account. Our favorites are bolded in the list below. To watch tutorial videos & check out our members' favorite alerts, see our article on the Top 4 Most Popular Account Security Alerts.

.png?width=650&name=Equation%20template%20blog%20(1).png)

- Remote Deposit Completed

- Automatic Deposit or Withdrawal Alert

- Balance Alert

- Debit Card Purchase Alert

- Insufficient Funds Alert

- Loan Payment Due Alert

- Transaction Alert

- Transfer Alerts

- Savings Goal Alerts

- OLB Access Alert

Choose a few that work best for your household finances and update your email/phone number so that you’re always in the know. For Copper State CU online banking, find this under Settings > Contact.

Budget Organizer Day 7:

What’s your financial net worth?

Financial Net Worth is the value of everything you own minus all your debts. This budget organizer item is interesting to calculate and see where you stand! You can also complete it for household finances rather than individually. We have a real-life example below (Monique) to help illustrate the process of determining net worth.

Asset: Money or Property You Own

Checking and savings account balances, value of securities (stocks/bonds), real property value, the market value of a car, etc.

Liability: Money You Owe

Mortgage loan balance, car loan balance, personal loan balance, credit card balance, student loan balance, etc.

To calculate, first find the value of all of your assets combined. Then subtract all of your loans or liabilities. The remaining number is your Financial Net Worth.

.png?width=449&name=10%20day%20budget%20tidy%20up%20checklist%20images%20(1).png)

Meet

Monique

Monique has $5,000 in her savings account, $300 in her checking account, $21,500 in a 401k, and owns her car free and clear (valued at $3,000). Plus she has a valuable heirloom piece of jewelry she stores in a safe worth $10,000. Her house's fair market value is $300,000. Her assets = $339,800.

Monique has $273,000 left to pay on her mortgage loan and carries a balance of about $6,000 in credit card debt. Her liabilities = $279,000

Monique's financial net worth = $60,800

What should my net worth be? A simple goal is to have a net worth that is increasing over time instead of decreasing, and that it's positive rather than negative. Some people prefer a target number though – and you can use this formula if you prefer:

.png?width=751&name=Equation%20template%20blog%20(3).png)

So – what’s your financial net worth?

If you aren't happy with it, you might want to check out our free budgeting template!

Budget Organizer Day 8:

Automate the Save

The three biggest reasons for not saving are:

- "I don’t know what to save for."

- "I don’t remember to save."

- "By the end of the month there’s nothing left for savings."

Let’s address solutions for all three:

“I don’t know what to save for.”

- At least $1000 in an emergency fund (it helps to open a separate savings account)!

- Periodic expenses like new tires, holidays, birthdays, etc.

- Build up a buffer fund in your checking account ($500) for times when cash flow gets low.

“I don’t remember to save.”

- Set up automatic transfers. Move money from checking to savings. If you’ll be tempted to take it back out, you can ‘hide’ the account from view (Copper State CU online banking gives you this option).

“By the end of the month there’s nothing left for savings.”

- Set up automatic transfers like the previous tip suggests, but do it ON PAYDAY. This is what people mean when they say "Pay Yourself First."

Budget Organizer Day 9:

Try Cash for Fun Money

This is easily the most impactful budget organizer item, because we all love spending money on things we enjoy. Whether it’s Top Golf, Anthem Outlets, dining out, or heading to northern Arizona for a summer vacation, many of us work hard and like to enjoy the money we earn by doing fun things or buying stuff for people we love.

This type of expenditure is hard to track if you’re using plastic money a.k.a. debit or credit cards. A very effective option is to visit the ATM every two weeks, on payday, and withdraw the exact amount that you’re budgeted to spend on fun stuff for the following two weeks. Keep the cash in your wallet, and then you don’t have any more you can spend until you visit the ATM on your next payday.

Even though so many of our purchases occur online now, you can easily make the cash system still work with online purchases. Just use your credit or debit card but immediately put the same amount of cash in an envelope that says ‘bank.’ Yes, it’s silly, but you’re still keeping track with cash by doing it this way. I recommend depositing the 'bank' cash back into your account weekly if you don't have a lot of extra cash in your credit union checking account.

Budget Organizer Day 10:

Be Kind

Be kind to yourself – keeping on top of your finances and your budget is a lot of work. Even if you only completed one or two of the tips from our 10-Day Budget Organizer, you’re still ahead of where you were before. (Or maybe you haven't done any of them yet because you're still reading this. 😅) Regardless, give yourself a kind word and a pat on the back for your efforts.

Be kind to others – Is there a charity or non-profit organization you’ve been wanting to support but never got around to it? Set up a donation schedule monthly or quarterly if that fits in with your budget and goals. Organizing your budget feels great, but so does helping others. ❤️

If you feel like you need more than a checklist to tidy up your budget, we've got you covered:

- Ultimate Budget Plan to Save You Time and Free Your Money eBook

- Free Budgeting Template - Excel Spreadsheet Download

1 CashBack Checking does not carry a monthly fee if member is enrolled in eStatements. For members who prefer paper statements, a $2 monthly fee will be assessed to their account, except for those members over the age of 65 or 17 years of age and younger.

This article is intended to be a general resource only and is not intended to be nor does it constitute legal advice. Any recommendations are based on opinion only. Rates, terms and conditions are subject to change and may vary based on creditworthiness, qualifications, and collateral conditions. All loans subject to approval.